Be prepared for a period of higher cost of capital

Productivity is the new priority and it replaces the growth strategy.

With interest rates rising in real terms, the value of growth strategies has declined. Managers need to look carefully at where they allocate capital, focusing more on investing in productivity. Nor should they treat strategy-making as a periodic exercise but rather as a dynamic, continuous process.

For most of the last 15 years, capital has been cheap. Since 2009, the after-tax cost of borrowing for some large companies has been below the rate of inflation, making their debt in real terms cost-free. And for much of this time, the stock market moved steadily upward, consistent with historically low costs of equity. We estimate that in early 2022, the weighted-average cost of capital (WACC) for the average company in the S&P 500 hovered below 6%.

All that changed in March 2022, when the world’s central banks began raising rates to curb rising inflation. Over the next 12 months, the U.S. Federal Reserve increased its benchmark Fed Funds rate from 0.25% to 4.75% and the yield on 10-year treasury notes climbed from 1.75% to almost 4% today. With rates on risk-free assets rising, the cost of debt for most large corporations also increased — from an average of less than 2.3% for most Baa-rated corporate debt in early 2022 to nearly 5.75% today. And, finally, the cost of equity capital also rose for most large companies over this period — from less than 7% to approximately 10%, according to research conducted by Aswath Damondaran at the Stern School of Business at NYU. All in, the WACC increased by 50% or more in just 12 months — from less 6% a year ago to nearly 9% today.

In the face of expensive capital, companies need to reexamine how they allocate their resources and communicate their strategies. In the brave new world of dearer capital this will involve:

1. Re-evaluating growth investments

We all know the obvious ways that growth can destroy value, like pursuing unprofitable business models or pushing products with negative gross margins. But profitable growth can destroy value too. This occurs when the capital that is invested in growth initiatives generates an accounting profit but does not produce a return on capital that exceeds the business’s cost of capital. In today’s world, leaders should be much more discerning about growth investments — doubling-down on investments that are likely to produce attractive returns and putting low-return growth investments on the backburner.

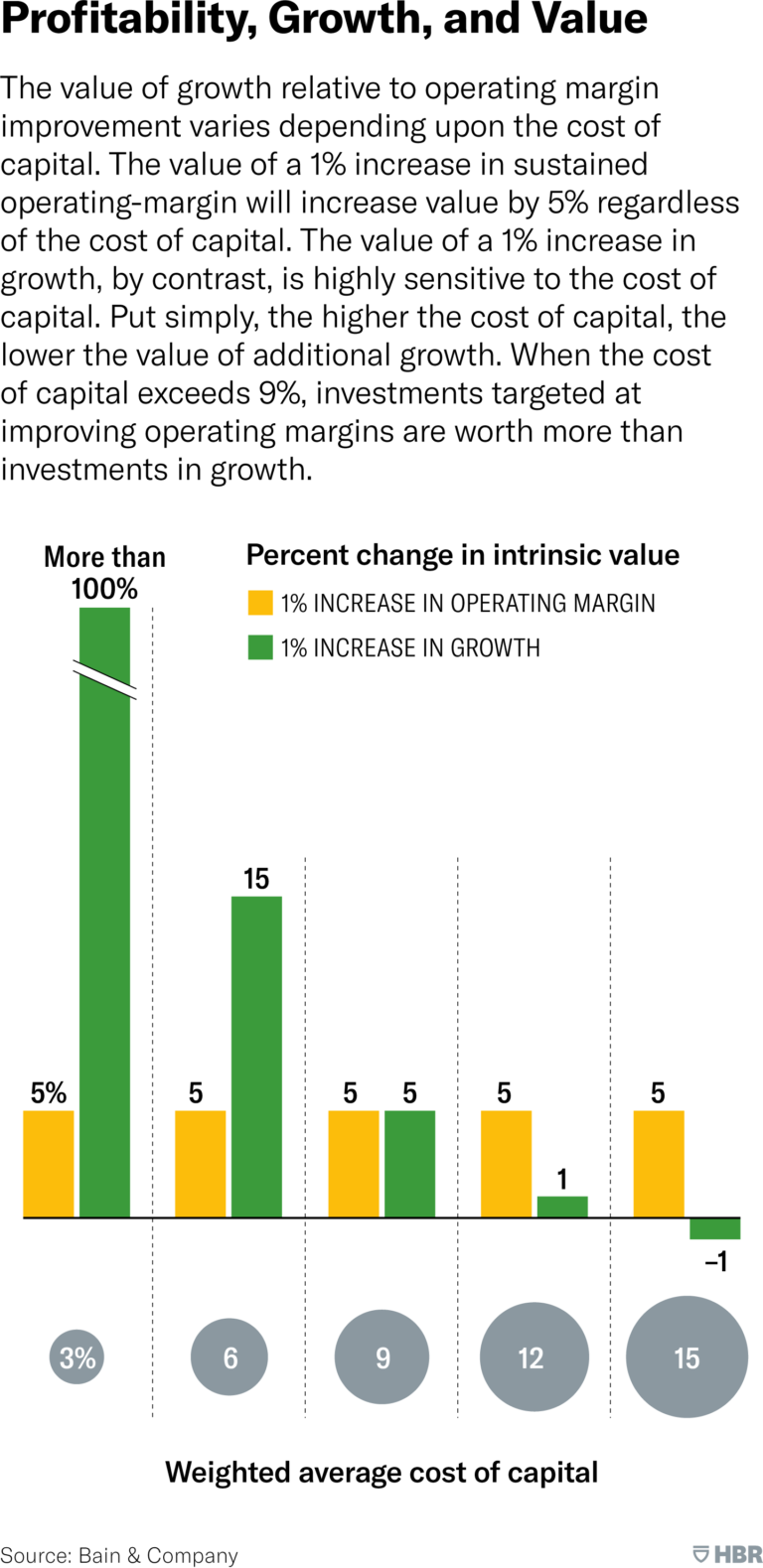

To elaborate, as capital costs rise, the value of growth relative to the value of margin improvement changes significantly (see the exhibit in this article). When the cost of capital is low, strategies that accelerate growth create far more value than those tied to boosting margins. This partially explains why so many companies pursued growth strategies over the last decade with considerable fanfare from investors — Adobe, Alphabet, Dell Technologies, even John Deere.

But as capital costs approach 9% or so (the current average for the S&P 500), the value of growth diminishes and strategies that increase profitability create more value. Many companies have already reached this tipping point. This is why the tech-heavy NASDAQ, comprised largely of growth stocks, declined so significantly last year — from a high of more than 14,000 in early 2022 to a low of 10,500 at the beginning of 2023 — and companies like Meta saw their market values collapse.

One company known for its focus on growth has begun describing its strategy and performance very differently in lieu of higher capital costs. The tech high-flier Netflix recently announced that it would end the company’s focus on “net subscriber adds” as a key performance metric. Indeed, despite adding more than 10 million new subscribers in 2022, Netflix is placing much greater emphasis on revenue, operating income, and operating margin as the company’s primary performance measures. The message to investors is clear: In assessing the value of Netflix, you must consider the profitability of streaming customers, not just their number. Other growth companies are likely to follow Netflix’s lead with this kind of messaging.

2. Investing in productivity

In anticipation of a slowing economy, more than 3,150 companies announced layoffs in 2022, according to data compiled by AI-powered market intelligence platform Intellizence. Amazon, Microsoft, Salesforce, Disney, and Philips led the way. In most cases, these layoffs were undertaken to increase efficiency, enabling each company to do the same, with less. In our experience, headcount actions can boost margins (at least temporarily), but they often make reigniting growth more challenging later — particularly if satisfying new demand requires significant rehiring. But the best companies find ways to increase productivity during slowdowns, not merely cut costs.

Boosting productivity requires that leaders identify the factors preventing their people from getting things done. In some instances, the problem is organizational complexity — that is, a combination of complex processes, organizational structures, and ways of working. Unless this underlying complexity is removed or otherwise dealt with, then any margin improvement will be short-lived. As one client executive recently remarked after overseeing her company’s third major workforce reduction in as many years: “We should have learned this by now. If you take the people out, but you don’t take the work out — or don’t change the way work gets done — the people will invariably come back.” Efficiency measures alone rarely create sustained improvements in profitability.

Enhancing productivity often requires investment — the substitution of capital or technology for labor. Some new technologies offer the potential to dramatically improve productivity, with modest investment. For example, AI-applications can enable many routine tasks to be automated. Advertising copy can be generated by machine rather than armies of marketing professionals; call centers can be manned by optimized language models, trained to respond to customers, suppliers, and other parties in a conversational way. Other technologies — most notably, factory automation — can require significant investment. But done right, technology investments reduce costs and increase productivity, allowing a company to improve margins in the short-term without sacrificing growth in the medium- to longer-term.

3. Dynamically reviewing capital spending plans

Most companies conduct capital planning on an annual basis. But the pace of change is necessitating a shift. CFOs need formal mechanisms to track changes in assumptions, risks, and opportunities continuously throughout the year. A plan to deploy capital midyear may need to be delayed, revised, or scrapped altogether, based on what takes place during the first half of the year.

Dynamic capital budgeting requires that organizations think about signposts, trigger points and related metrics. Signposts refer to the critical market and competitive factors that most influence a company’s decision to deploy capital. For example, a critical assumption behind General Motor’s decision to invest heavily behind Battery Electric Vehicles (BEVs) was the rate of penetration of BEVs in the market. That number is driven by a few specific signposts — such as, the cost of batteries, changes in government mandates, availability of charging stations, competitor pricing actions, etc.

Each of these signposts has important trigger points that should impact the assumptions built into the capital plan. For example, if the number of charging stations in major metropolitan areas does not grow as anticipated this year, then the assumptions in GM’s capital plan would most probably need to change. By continuously monitoring signposts — relative to trigger points — companies can determine if (and when) they need to modify their capital plans to stay ahead of the competition.

The age of cheap money is over. In the face of rising capital costs, leaders should rethink their approach to resource allocation and capital planning. These processes must become more disciplined and dynamic. Once “obvious” investments in growth may need to be reconsidered. And actions to improve margins must be mindful of productivity, not just efficiency. Capital — and its costs — must be measured and carefully managed. Otherwise, companies risk over-investing in the wrong opportunities and under-investing in the right ones, undermining future profitability, growth, and value creation.

As this table shows, while the impact on value (y axis) of a 1% increase in the operating margin generated by improved productivity remains constant (at 5% of company value) no matter what the cost of capital is, (x axis) the impact on company value of a 1% increase in the company’s growth is highly sensitive to the cost of capital. Put simply, the higher the cost of capital is, the less valuable is an increase in revenues, and when the cost of capital exceeds 9%, investments in productivity become more valuable than investments in growth.

***

Alessio De Filippis, Founder and Chief Executive Officer @ Libentium.

Founder and Partner of Libentium, developing projects mainly focused on Marketing and Sales innovations for different types of organizations (Multinationals, SMEs, startups).

Cross-industry experience: Media, TLC, Oil & Gas, Leisure & Travel, Biotech, ICT.